Introduction

Financial freedom isn’t just about having money in the bank—it’s about having the power to make life decisions without being overly stressed about finances. It’s the ability to pay your bills on time, save for emergencies, invest in your future, and still have enough to enjoy life’s precious moments.

For many Nigerians, achieving financial freedom can seem like a distant dream, especially with rising costs of living and economic uncertainties. However, the path to financial independence isn’t reserved for the wealthy elite or those with six-figure salaries. With discipline, smart planning, and the right financial partner, anyone can build a solid foundation for lasting prosperity.

In this comprehensive guide, we’ll walk you through five practical steps that will transform your relationship with money and set you on the path to financial freedom. Whether you’re just starting your career, running a small business, or looking to secure your family’s future, these strategies will help you take control of your finances and build the life you’ve always wanted.

Step 1: Define Your Financial Goals

Why Goal-Setting Matters

You can’t reach a destination if you don’t know where you’re going. Financial goals give your money a purpose and provide the motivation you need to make smart financial decisions daily. Without clear objectives, it’s easy to spend impulsively and wonder where your money went at the end of each month.

Types of Financial Goals

Short-term goals (1-2 years):

- Building an emergency fund of 3-6 months’ expenses

- Paying off high-interest debt

- Saving for a new phone, laptop, or household item

- Funding a vacation or special celebration

Medium-term goals (3-5 years):

- Saving for a car down payment

- Starting a small business

- Funding professional certifications or courses

- Renovating your home

Long-term goals (5+ years):

- Buying property or land

- Children’s education fund

- Building a retirement nest egg

- Achieving complete financial independence

How to Set Effective Financial Goals

Use the SMART framework to create goals that work:

Specific: Instead of “I want to save money,” say “I want to save ₦1,200,000 for a plot of land.”

Measurable: Track your progress with concrete numbers. “Save ₦100,000 monthly” is measurable.

Achievable: Be realistic about what you can accomplish with your current income. Stretch yourself, but don’t set impossible targets.

Relevant: Your goals should align with your values and life priorities. Don’t save for a luxury car if what you truly need is business capital.

Time-bound: Set deadlines. “Save ₦1,200,000 within 12 months” creates urgency and focus.

Take 30 minutes this week to write down your top three financial goals in each category (short, medium, and long-term). Be specific about the amount needed and your target date. Share these goals with an accountability partner—your spouse, trusted friend, or financial adviser—who will check in on your progress.

Practical Exercise

Step 2: Track Your Income and Expenses

The Foundation of Financial Awareness

You cannot manage what you don’t measure. Most people significantly underestimate how much they spend on non-essentials. Tracking your money flow reveals spending patterns, identifies financial leaks, and empowers you to make informed decisions.

Understanding Your Cash Flow

Income sources: Document all money coming in—salary, business profits, side hustles, rental income, dividends, and gifts. Know your exact monthly income after taxes.

Fixed expenses: These are predictable monthly costs like rent, loan payments, school fees, insurance premiums, and utility bills.

Variable expenses: These fluctuate monthly—food, transportation, entertainment, clothing, and personal care.

Irregular expenses: Quarterly or annual costs like vehicle maintenance, property taxes, or professional memberships.

Tracking Methods That Work

Traditional method: Keep a small notebook where you record every expense daily. This physical act creates awareness and accountability.

Digital tracking: Use budgeting apps like Cowrywise, PiggyVest, or simple Excel spreadsheets. Many Nigerian banks now offer spending analysis in their mobile apps.

The envelope system: Withdraw cash for specific budget categories and place them in labeled envelopes. When the envelope is empty, spending stops for that category.

Hybrid approach: Use digital payments for tracking purposes, but review your spending weekly in a dedicated 15-minute session

The 50/30/20 Budget Rule

A simple framework that works for most people:

- 50% of income: Needs (housing, food, transportation, utilities, insurance)

- 30% of income: Wants (dining out, entertainment, hobbies, subscriptions)

- 20% of income: Savings and debt repayment

Adjust these percentages based on your goals and life stage. If you’re aggressively saving for a home, you might aim for 30% savings by reducing wants to 20%.

Common Money Leaks to Watch

Studies show that small, frequent purchases add up significantly:

- Daily snacks and drinks (₦1,000/day = ₦30,000/month)

- Unused subscriptions (streaming services, gym memberships)

- Bank charges and unnecessary fees

- Impulsive online shopping

- Excessive data purchases

- Food waste from poor meal planning

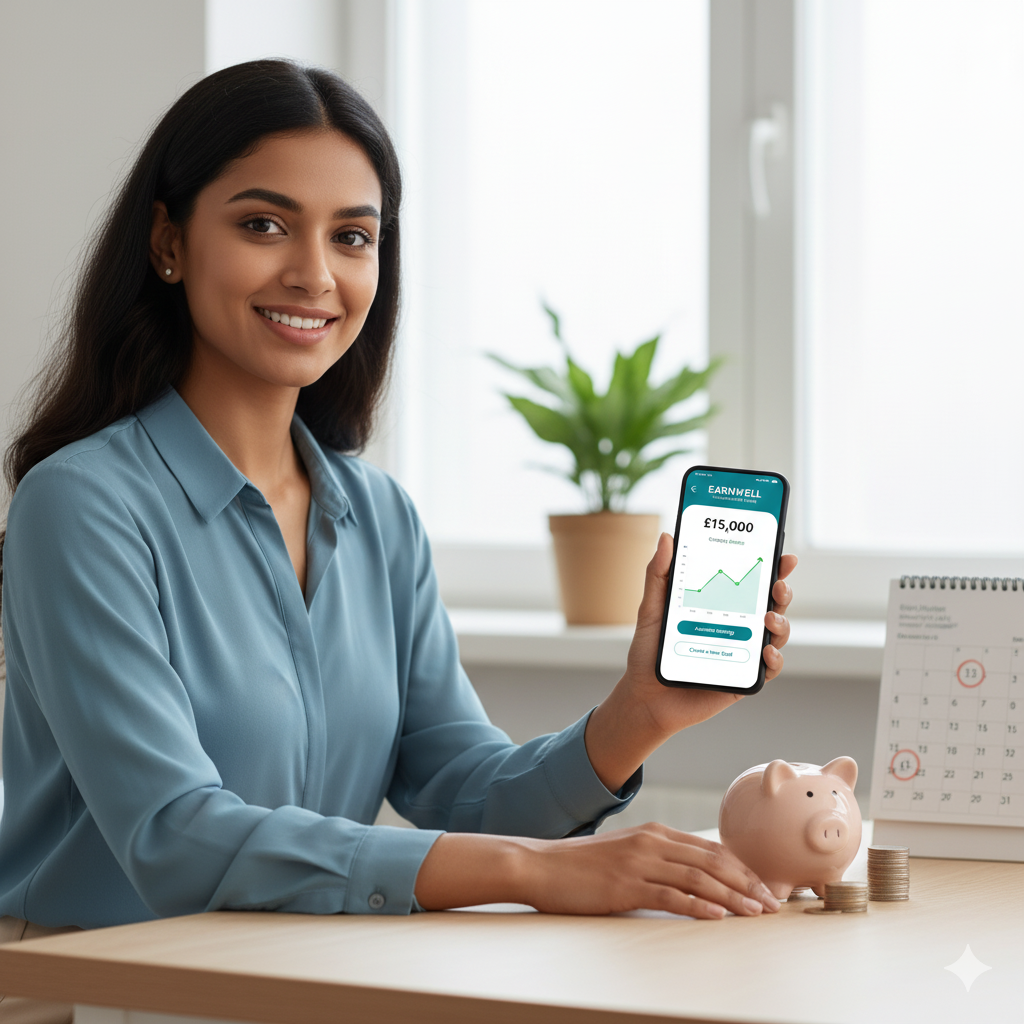

Step 3: Save Consistently with Earnwell Microfinance Bank

Why Consistent Saving Transforms Your Financial Life

Saving isn’t what you do with money left over after spending—it’s what you do first. Consistent saving builds wealth through the power of compound growth, creates a financial safety net, and gives you peace of mind knowing you can handle unexpected expenses.

The Psychology of Saving

Most people struggle with saving because they rely on willpower alone. The key is to make saving automatic and effortless. When saving happens before you see or touch the money, you adapt your lifestyle around what remains.

How Earnwell Microfinance Bank Makes Saving Easy

Competitive interest rates: Your savings grow faster with attractive returns that beat inflation, ensuring your money maintains its purchasing power over time.

Flexible savings plans: Whether you prefer daily, weekly, or monthly contributions, Earnwell offers savings products tailored to your income pattern and financial goals.

Automated savings: Set up standing orders that automatically transfer funds from your current account to your savings account on payday. This “pay yourself first” strategy removes temptation and builds discipline.

Target savings accounts: Create dedicated accounts for specific goals—your emergency fund, children’s education, business expansion, or dream vacation. Seeing progress toward concrete objectives keeps you motivated.

Locked savings options: For those who struggle with dipping into savings, fixed-term deposits with withdrawal restrictions help you maintain discipline while earning higher interest rates.

Accessible customer service: Earnwell’s dedicated team provides personalized guidance, helping you choose the right savings product and adjust your strategy as your circumstances change.

Building Your Emergency Fund First

Before investing or tackling long-term goals, establish an emergency fund of 3-6 months’ living expenses. This financial cushion prevents you from going into debt when unexpected costs arise—medical emergencies, job loss, vehicle repairs, or family crises.

Calculate your monthly essential expenses (not including wants) and multiply by three for a starter emergency fund, or by six for a more robust safety net. Keep this money in a high-yield savings account with Earnwell where it’s accessible but separate from your everyday spending money.

The Power of Compound Interest

When you save consistently and earn interest, you don’t just grow your principal—you earn returns on your returns. For example:

If you save ₦50,000 monthly in an account earning 10% annual interest:

- After 1 year: ₦630,000 (you saved ₦600,000, earned ₦30,000)

- After 5 years: ₦3,870,000 (you saved ₦3,000,000, earned ₦870,000)

- After 10 years: ₦10,230,000 (you saved ₦6,000,000, earned ₦4,230,000)

The longer your money works for you, the more powerful compound growth becomes.

Making Saving a Non-Negotiable Habit

Start with what you can: Even ₦5,000 or ₦10,000 monthly is a legitimate start. As your income grows, increase your savings proportionally.

Automate the process: Schedule automatic transfers to occur immediately after payday, before you have a chance to spend the money.

Save windfalls: Commit to saving at least 50% of unexpected income—tax refunds, bonuses, gifts, or side income.

Celebrate milestones: When you reach savings goals, acknowledge your progress. This positive reinforcement strengthens the saving habit.

Review and adjust: Quarterly, evaluate your savings rate. Can you increase it by 2-5%? Small incremental improvements create significant long-term results.

Step 4: Invest Wisely

From Saving to Wealth Building

Saving isn’t what you do with money left over after spending—it’s what you do first. Consistent saving builds wealth through the power of compound growth, creates a financial safety net, and gives you peace of mind knowing you can handle unexpected expenses.

Understanding Investment Basics

Risk and return relationship: Generally, higher potential returns come with higher risk. Your investment strategy should balance growth potential with your risk tolerance and time horizon.

Diversification: Don’t put all your eggs in one basket. Spreading investments across different asset classes reduces overall risk.

Time horizon: Investments should match your timeline. Money needed within 3 years shouldn’t be in volatile assets; long-term goals can weather short-term market fluctuations.

Inflation protection: Your investments should at minimum outpace inflation (typically 10-15% in Nigeria), or your purchasing power decreases over time.

Investment Options for Nigerian Investors

Treasury Bills and Bonds: Government securities offer relatively safe, predictable returns (10-18% annually). Ideal for conservative investors or short to medium-term goals.

Fixed Deposits: Offered by banks and microfinance institutions like Earnwell, these provide guaranteed returns with NDIC insurance protection (up to ₦5,000,000).

Real Estate: Property investment offers rental income and capital appreciation. Start with affordable land purchases in developing areas, or pool resources with trusted partners for larger projects.

Stocks and Equity Funds: Buy ownership in Nigerian companies through the stock market. While more volatile, equities historically provide the highest long-term returns (15-25% annually over time).

Mutual Funds: Professional fund managers invest your money across diversified portfolios. Good for beginners who lack time or expertise to manage investments directly.

Agricultural Investments: Agric-tech platforms offer opportunities to invest in specific farming projects with projected returns of 15-30% over 6-12 months.

Small Business Investment: Start or expand your own business, or become a silent partner in profitable ventures within your network.

Skills and Education: Investing in yourself through courses, certifications, and skill development often yields the highest returns through increased earning capacity.

Investment Principles for Success

Start early: Time is your greatest investment advantage. A 25-year-old saving ₦30,000 monthly will have more at retirement than a 35-year-old saving ₦60,000 monthly, due to compound growth.

Be consistent: Regular investing (monthly contributions) smooths out market volatility and builds discipline. Don’t try to time the market.

Think long-term: Avoid panic selling during market downturns. Historically, markets recover and grow over extended periods.

Educate yourself: Read investment books, follow financial news, attend seminars. Knowledge reduces anxiety and improves decision-making.

Seek professional advice: Consult with financial advisers, especially for significant investments. At Earnwell Microfinance Bank, experts can guide you toward suitable investment products aligned with your goals and risk profile.

Avoid get-rich-quick schemes: If returns sound too good to be true, they probably are. Ponzi schemes and fraudulent investment platforms have destroyed countless Nigerians’ wealth.

Creating Your Investment Plan

- Define your investment objectives and time horizons

- Assess your risk tolerance honestly

- Allocate your investment capital across asset classes

- Start with simple, understood investments

- Gradually diversify as you gain knowledge and confidence

- Review and rebalance your portfolio annually

- Stay disciplined during market volatility

Remember: investing is a marathon, not a sprint. Consistent, patient investing beats aggressive, emotional decision-making every time.

Remember:

Step 5: Increase Your Income

The Ceiling-Breaking Strategy

Financial freedom rarely comes from a single income source. The wealthy typically have 5-7 income streams. Diversifying income protects you from economic shocks and accelerates wealth accumulation.

Career Income Enhancement

Skill development: Acquire high-demand skills in your industry. Digital marketing, data analysis, project management, and technical skills command premium salaries.

Professional certifications: Relevant credentials often translate to immediate salary increases of 20-40%.

Strategic job moves: Loyalty to undervaluing employers hurts your wealth-building. Research market rates for your role and negotiate or transition strategically.

Performance excellence: Become indispensable by consistently exceeding expectations. Top performers receive bonuses, promotions, and opportunities others miss.

Networking: Many high-paying opportunities come through professional relationships. Attend industry events, join professional associations, and maintain meaningful connections.

Side Hustle and Business Opportunities

Monetize existing skills: Graphic design, writing, photography, tutoring, consulting, hairdressing—you likely have marketable skills waiting to be monetized.

Online businesses: E-commerce, digital products, affiliate marketing, and content creation offer flexible income opportunities with low startup costs.

Service businesses: Cleaning services, event planning, catering, logistics—service businesses can start small and scale without massive capital.

Trading and retail: Buy products wholesale and resell at profit. Start with items you understand and markets you can access easily.

Freelancing platforms: Upwork, Fiverr, and local platforms connect your skills with paying clients globally.

Rental income: Rent out spare rooms, parking spaces, equipment, or vehicles you’re not fully utilizing.

Passive Income Development

Dividend-paying investments: Stocks and real estate that generate regular income without active work.

Digital products: Create once, sell repeatedly—ebooks, courses, templates, stock photos, or software.

Rental properties: Real estate generating monthly rental income after initial investment.

Royalties: Write books, create music, or develop intellectual property that pays ongoing royalties.

Strategic Income Growth Plan

Assess current earning capacity: What’s your market value? Are you underpaid compared to industry standards?

Identify high-leverage opportunities: Which income-increasing activities offer the best return on time invested?

Invest in income-generating skills: Allocate time and money to learning skills that directly boost earning potential.

Start small with side income: Begin with manageable projects that don’t compromise your primary job performance.

Systematize and scale: Once a side income stream proves viable, create systems that allow growth without proportional time increases.

Reinvest earnings: Initially, channel increased income toward debt elimination and investment rather than lifestyle inflation.

Avoiding Income-Growth Traps

Lifestyle inflation: As income rises, expenses shouldn’t rise proportionally. Maintain moderate living standards while savings and investments grow.

Burnout: Multiple income streams shouldn’t destroy your health or relationships. Sustainable wealth-building preserves your wellbeing.

Tax negligence: Higher income means tax obligations. Work with accountants to structure income tax-efficiently and avoid penalties.

Quality over quantity: Three well-managed income streams typically outperform seven poorly managed ones.

Creating Your Financial Freedom Action Plan

Your 90-Day Quick-Start Guide

Your Financial Freedom Is Within Reach

Financial freedom isn’t about becoming a millionaire overnight—it’s about making consistent, smart decisions that compound over time into life-changing results. Every wealthy person you admire started exactly where you are now: at the beginning.

The five steps outlined in this guide—defining clear goals, tracking your money, saving consistently with Earnwell Microfinance Bank, investing wisely, and increasing your income—form a proven blueprint that has worked for millions of people worldwide. These aren’t theoretical concepts; they’re practical strategies you can implement starting today.

What sets successful wealth builders apart isn’t access to secret information or special advantages—it’s simply commitment to the process and consistency in execution. Your first step might be opening a savings account, your second might be tracking expenses for one week, and your third might be reading one investment book. Each small action moves you closer to financial independence.

Earnwell Microfinance Bank stands ready to partner with you on this journey, offering not just financial products but personalized guidance, competitive returns, and the support you need to stay on track toward your goals. Whether you’re saving your first ₦10,000 or your tenth million, you’ll find a partner committed to your financial success.

The question isn’t whether you can achieve financial freedom—you absolutely can. The question is: will you start today? Your future self will thank you for the decision you make right now.

Take the first step: visit Earnwell Microfinance Bank today, open your savings account, and begin your journey to the financial freedom you deserve.

Summary

This comprehensive guide to financial freedom outlines five proven steps for building lasting wealth: defining clear SMART financial goals, tracking income and expenses to identify money leaks and optimize spending, saving consistently with high-yield accounts at Earnwell Microfinance Bank to harness compound interest, investing wisely across diversified asset classes to grow wealth beyond inflation, and strategically increasing income through career advancement and side businesses. By implementing these practical strategies with discipline and partnering with Earnwell Microfinance Bank for accessible savings solutions and expert financial guidance, Nigerian families and professionals can break free from financial stress, build emergency funds, invest for long-term goals, and achieve true financial independence. Start your journey to financial freedom today with Earnwell—your trusted partner in wealth creation and financial security.